Our Products

Our Services

Know what is creditworthiness, its importance, what factors determine it and how to improve your creditworthiness.

Last updated on: Jun 15, 2026

Creditworthiness is defined as a metric that gauges how well you have managed your credit as well as debt obligations thus far. By way of analysing your credit report, a creditor can gauge your repayment history. Based on your creditworthiness, the borrower will decide whether or not to approve your loan request. By making your payments on time, and not defaulting, you can ensure that you maintain and improve your creditworthiness.

Now that we have shed light on the creditworthiness meaning, we shall delve further into who measures your creditworthiness. To assess your creditworthiness, follow these key steps:

Start by accessing your credit report from a recognised credit bureau in India, such as TransUnion CIBIL, Experian, Equifax, or CRIF High Mark. Most bureaus offer one free report per year through their official websites.

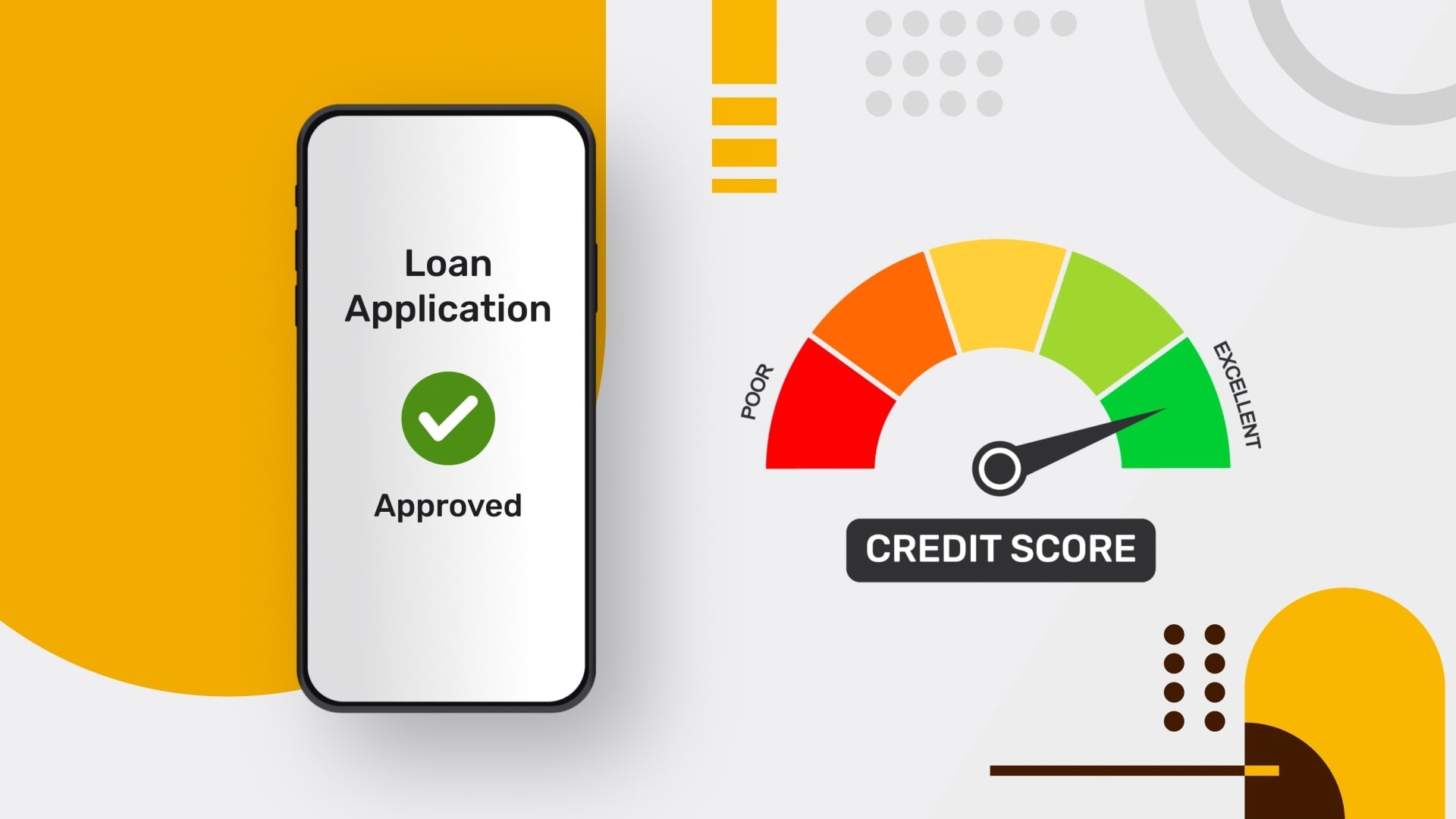

Check your CIBIL score carefully. A higher score (typically 750 and above) indicates strong creditworthiness, improving your chances of loan approval at better interest rates.

Go through your past repayment records for loans and credit cards. Ensure there are no delays, defaults, or missed payments, as these significantly impact your creditworthiness.

Evaluate how much of your available credit you are using. A high credit utilisation ratio (generally above 30%) can signal financial stress and negatively affect your score.

Your CIBIL score is a key numerical indicator of your creditworthiness, helping lenders evaluate your ability to repay loans and manage credit responsibly. A higher score generally reflects stronger financial discipline and increases your chances of securing loans with favourable terms.

| CIBIL Score Range | Creditworthiness Level | What It Indicates |

|---|---|---|

300 – 549 |

Poor |

High risk borrower; loan approvals are difficult, and interest rates are typically high |

550 – 649 |

Fair |

Moderate risk; limited approval chances with stricter terms and higher rates |

650 – 749 |

Good |

Relatively reliable borrower; better chances of loan approval with reasonable terms |

750 – 900 |

Excellent |

Highly creditworthy; easier approvals, lower interest rates, and higher credit limits |

Creditworthiness can be defined by a range of factors, as elucidated below:

The creditworthiness of a borrower is determined, to a great extent, by their timeliness of payments – when it comes to credit card bill payments and loan repayments. If you default on a payment or delay in the same, it can adversely affect your CIBIL score.

Additionally, if you take a longer time to repay your outstanding dues, and if the number of your unpaid bills piles up, your credit score will fall. Your repayment history contributes to 30% of your credit score. Hence, you must make sure that you repay your dues on time, and do not default on the same.

Another important factor that determines your creditworthiness is your credit utilisation. This factor makes up 25% of your credit score. Additionally, if a certain borrower showcases poor spending habits, like ending beyond your means, can also result in a higher ratio of credit utilisation, which can bring down the credit score. When it comes to sanctioning a loan, lenders tend to view a higher rate of credit utilisation as a negative indicator of a consumer’s financial behaviour.

Before approving a loan request, all lenders necessarily check a borrower’s credit report to assess if there is a new enquiry, new loan request, or a new credit card request. This is a deciding factor, as it helps determine the repayment ability of the borrower. If a borrower applies for multiple loans or credit cards on a routine basis, this is a sign that the borrower may not be able to meet the repayment terms and conditions set by the lender. If you, as a borrower, make multiple and frequent credit inquiries, your credit score can be impacted by up to 20%.

If you have a long, and stable credit history, it has a positive impact on your credit score, and makes accessing a loan much easier for you. All lenders in the market will be more than willing to approve loans to you if consistent repayment history, over a long duration. Thus, it is advisable to not close old credit cards, even if not used that much and to keep them active to maintain your credit score.

Before approving a loan, a lender will typically check your credit mix of both unsecured and secured loans. Secured loans refer to loans wherein you must offer assets as collateral, such as home loans and car loans. Unsecured loans are loans that do not need any collateral, such as personal loans.

Understand how creditworthiness impacts your borrowing capacity and terms. Here’s why it matters before applying for credit:

Understanding the meaning of creditworthiness is essential, as it reflects your ability to repay borrowed funds and directly influences lenders’ decisions.

Lenders assess your creditworthiness to approve or reject loan and credit card applications, making it a key factor in accessing credit.

A higher creditworthiness can help you secure loans at lower interest rates, while a lower score may result in higher borrowing costs.

Your creditworthiness also determines your credit limit, affecting how much you can borrow through credit cards or loans.

Even if you do not plan to apply for credit immediately, maintaining a good CIBIL score ensures easier access to financial and select non-financial services in the future.

You can regularly monitor your credit score through authorised credit bureaus or financial platforms to stay informed and take corrective action if needed.

Understanding creditworthiness helps you take the right steps to improve it. Have a look at the approaches below to know how you can strengthen your credit profile:

You must first start by tackling all accounts that are past due, as well as all debt collections. If you manage to pay these off, your credit score will improve dramatically.

Ensure that moving forward, you make all your payments on time. If you do not have an active account, you may wish to add another credit card, which will vastly improve your creditworthiness.

When it comes to outstanding loans, try your level best to make bigger down payments. This translates to the lender taking on lesser risk, and can hence help you get approved for a car loan or even a mortgage, in spite of average credit scores.

If you wish to increase your chances of getting approved for a loan, having a co-signer can help. If you default on the payment of your loan, this co-signer is responsible for completing the payments on your behalf.

Here are a few real-life scenarios that illustrate the meaning of creditworthiness across various individuals and impacts borrowing outcomes:

A salaried individual with a CIBIL score of 800, stable income, and no missed payments. Such a borrower is likely to get loan approvals quickly, with lower interest rates and higher credit limits.

A self-employed individual with a CIBIL score of 620 and two instances of late payments may face stricter loan terms, higher interest rates, or even rejection due to perceived higher risk.

A borrower with moderate income, a decent credit mix, and consistent repayments (score around 700–750) may still qualify for loans, but the offered terms may not be as favourable as those given to high-score applicants.

Reviewer

Creditworthiness refers to your ability and reliability to repay borrowed money. It indicates how likely you are to meet loan or credit obligations on time.

Creditworthiness is determined by factors such as your credit score, repayment history, income stability, outstanding debts, and overall financial behaviour. Lenders assess these before approving loans or credit.

The 5 C’s of creditworthiness are:

Character – your credit history and repayment behaviour

Capacity – your ability to repay using income and cash flow

Capital – your savings and assets

Collateral – security pledged against the loan

Conditions – external factors such as economic environment, loan purpose, and prevailing market conditions that may impact repayment ability

Your creditworthiness matters because it directly affects loan approvals, interest rates, and credit limits. Higher creditworthiness increases your chances of accessing credit on better terms.

The five key factors of creditworthiness include:

Payment history – record of timely repayments

Credit utilisation ratio – how much of your available credit you use

Length of credit history – how long you’ve maintained active accounts

Credit mix – variety of credit types like loans and cards

New credit enquiries – frequency of recent credit applications

Pay all EMIs and credit card bills on time, keep credit utilisation below 30%, avoid frequent loan applications, and maintain a healthy mix of secured and unsecured credit. Regularly review your credit report for errors and clear outstanding dues promptly to steadily improve your creditworthiness over time in India effectively.