A ULIP or a Unit-Linked Insurance Plan is a popular financial instrument that offers the dual benefits of insurance and investment. Here, the main goal is to furnish a life cover for the policyholder, along with investments in various funds to create wealth. While a part of your premium is dedicated to insurance, the rest of your money is invested in equity, debt, or combinations of both to generate wealth over the long term. ULIP returns are market-linked, hence assessing the interest you would earn in 10 years can be challenging. However, this article illustrates how to get an estimate of your ULIP plan return.

How to Assess ULIP Returns in 10 Years?

We bring you two efficacious methods to compute your ULIP returns in 10 years. You can choose to calculate your ULIP returns by ‘Absolute returns’ if your investment tenor is up to a year. However, if the returns are for more than a year, you can select the CAGR method.

Absolute Returns

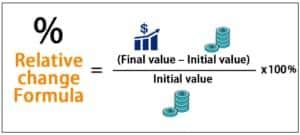

To calculate absolute returns, you must have the initial and current Net Asset Value (NAV). Net Asset Value is a fund’s asset value minus the value of its liabilities. This value will help you determine if the fund is overvalued or undervalued. In other words, it is the overall cost of a mutual fund that depends on the price per unit fund.

You must follow the following steps

From your current NAV, subtract your initial NAV

Divide the received value from your initial NAV

Multiply it with 100 to receive your value in %

The mathematical formula for absolute returns is:

This method proves effective while computing ULIP returns for a small period. For example, the Net Asset Value may change over longer periods, consequently changing the absolute returns.

CAGR (Compounded Annual Growth Rate)

Your annual growth over a specific period can be computed with the help of CAGR. To calculate your compound annual growth rate, you must follow the correct mathematical formula, which is denoted as:

Here, you have to use the beginning and ending value of your scheme, in addition to the invested years. Divide the ending value with the beginning value and multiply it 1/nth the number of years you will be investing for. Multiply your value with 100 to get % value.

The mean annual growth rate is calculated but it does not consider the volatile market behaviour between the invested years and is a completely historical value. Thus, even if your value has been increasing over the last 5 years, you cannot predict the outcome and assume the wealth growth at the same rate for the remaining duration of your investment.

These effective methods can surely help you with computing your ULIP returns. All you have to do is follow the given steps to avoid any complications. However, it must be understood that the value after computation is just an ‘idea’, and not the exact value of your returns.

What Makes ULIP the Best Investment Product for Wealth Generation in 10 Years?

Helps Meet Long-Term Goals:

ULIPs are considered as the best instruments of investment when you aim to meet long-term goals like planning for your retirement or saving for your child’s education. The IRDAI (Insurance Regulatory and Development Authority of India) has changed the lock-in period of ULIPs from 3 years to 5 years, thus inculcating financial discipline and allowing your funds the time to grow and multiply over time.

Active or Passive Fund Management:

Usually, you will be spared the hassle of tracking your investments as each company has its own fund manager that looks over the investments. However, you can also take up a hands-on approach and be actively involved in how your funds are allocated.

Flexibility to Switch and Redirect Premiums:

According to market performance and your risk appetite, you can switch between equity and debt-based portfolios. You can also invest in balanced funds with a combination of both equity and debt. This flexibility is a major factor why ULIPs are popular.

Now that you’ve understood the various reasons why ULIPs are the best financial instruments, it’s important that you understand the factors that influence your ULIP plan returns.

There are 2 main factors that can influence your ULIP returns in 10 years. They are:

ULIP Charges

While investing in ULIPs, you are liable to pay certain charges based on the company policy, which may vary from one another. Normally, mortality charges, fund management charges, admin charges, and premium allocation charges are levied on the policyholder. Upon maturity, such charges will be deducted from your fund value before it is disbursed to you. Thus, ULIP charges can affect your returns. The IRDAI has, however, protected the policyholder from obscenely high charges, by putting a cap on the fees that can be levied by insurance providers.

Market Performances

How the market performs during your investment will majorly dominate your ULIP returns in 10 years. Hence to maximise your ULIP returns, it is recommended that you do a historic performance check, i.e. ULIP returns in the last 10 years, to get some indications before making any investment decisions.

Conclusion

The ULIPs you opt for can help generate a handy corpus that can, in turn, be useful for the goals of you and your loved ones. While you create wealth, the life cover also helps protect this wealth. Thus, it is important that you ensure and select an appropriate plan that supports you and your family.

On Bajaj Markets, you can choose a plan that provides high returns and an optimum amount of life coverage. You can choose from Child Plans, Retirement Plans, and Investment Pl on Bajaj Markets. You can also switch your funds according to your risk appetite, investment horizon and changing market movements. With features like multiple portfolio management options and ULIP tax benefits, choose Bajaj Allianz ULIP Plans and start building your future now!

ULIP Top Pages

- Advantages of Investing in ULIP

- Balanced funds

- Bond Funds

- Fund Switching Techniques

- Lock in period in ULIPs

- Mortality charges in ULIPs

- Myths about ULIPs

- Things to consider before buying ULIPs

- ULIP vs Mutual Funds

- ULIP vs PPF

- ULIP vs SIP

- What is ULIP?

- Why invest in ULIPs?

- ULIP tax benefits

- Type 1 and Type 2 ULIPs

- ULIP vs ELSS

- Pension Calculator

- Ulip Charges You Must Know

- Pension Plan Guide

- Retirement Calculator

- ULIP Fees & Charges

- Types Of ULIP

- ULIP Quote

ULIP in Depth

- How to make a personalized investment plan

- How to choose the best ULIP plan

- Importance of Asset Allocation

- ULIP charges you should know

- Ultimate guide to ULIPs

- Importance of market linked instruments

- Evolution of ULIPs

- All about Endowment Plans

- ULIP NAV and its calculation

- Benefits of LLG

- ULIP FAQs

- ULIP fund performance

- Long Term Capital Tax on ULIPs

- Features and Benefits of Child ULIPs

- ULIP as an Investment Option

- How To Invest In ULIP At Low Costs

- Young Professional Guide To Investing In ULIP

- Benefits Of Online ULIPs Over Offline Ulips

Government Investment Schemes

FAQs on ULIP Returns

Do ULIPs offer higher returns?

ULIPs offer higher returns as compared to low-risk investment options.

Is ULIP a long-term financial instrument?

Yes, ULIPs are a long-term investment option.

Is ULIP maturity tax free?

Yes, ULIP returns are exempted from tax under Section 10(10D) of the Income Tax Act, 1961.

What is the full form of ULIP?

The full form of ULIP is Unit-Linked Insurance Plan.

Does ULIP offer any tax benefits?

Yes. You can avail income tax deduction under Section 80C of the Income Tax Act on premiums paid towards ULIP.

Explore

Related Product