Our Products

Our Services

Table Of Content

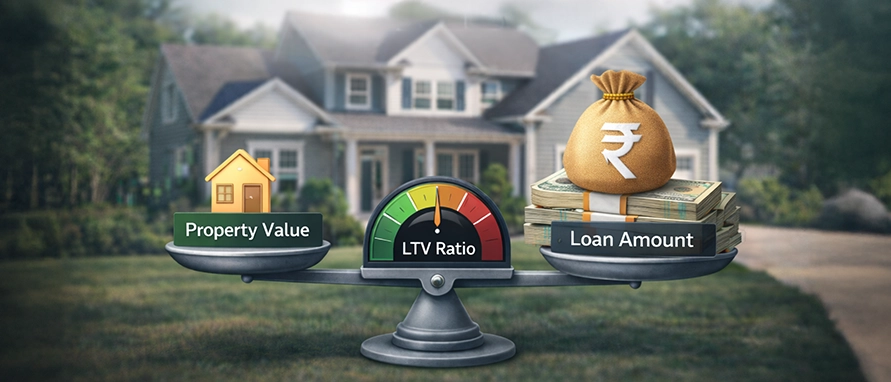

When considering a loan, most people only factor in the interest rate, while overlooking other equally, if not more, important factors. One such factor is loan-to-value (LTV). The LTV for loan against property directly controls how much capital you can unlock from your asset without liquidating it. A higher ratio improves liquidity, supports larger financial goals, and reduces the need for parallel borrowing. Therefore, comparing lenders only on rates misses a crucial dimension that materially impacts your loan strategy, cash flow planning, and risk exposure.

This guide focuses on how lenders stack up when you evaluate a loan against your property through the lens of loan-to-value flexibility, tenure comfort, and funding scale, rather than promotional claims.

Lenders across NBFCs, housing finance companies, and financial institutions broadly follow similar regulatory limits for loan-to-value calculations. However, they may offer different loan sizes, tenure support, and fee structures, which indirectly affect how useful the sanctioned LTV becomes in real terms. While lender-specific ratios remain undisclosed publicly, most institutions extend financing up to 75-80% of the assessed property value, subject to internal risk policies.

The table below helps you assess lenders based on parameters that influence how effectively the LTV for loan against property translates into usable funding.

Lender |

Starting Interest Rate (p.a.) |

Max Loan Amount |

Max Tenure |

8.99% |

₹5 Crores |

216 months |

|

9.25% |

₹15 Crores |

240 months |

|

14.00% |

₹50 Lakhs |

240 months |

|

10.60% |

₹5 Crores |

180 months |

|

13.90% |

₹20 Lakhs |

180 months |

|

14.75% |

₹1 Crore |

180 months |

|

15.00% |

₹30 Lakhs |

240 months |

|

9.45% |

₹7.5 Crores |

180 months |

|

9.75% |

₹10 Crores |

144 months |

|

14.00% |

₹1 Crore |

180 months |

|

9% |

₹10 Crores |

180 months |

|

10.50% |

₹10 Crores |

180 months |

|

14.00% |

₹25 Lakhs |

180 months |

|

22.00% |

₹15 Lakhs |

180 months |

*Processing fees and rates vary by borrower profile and property type.

Disclaimer: Interest rates, tenures, and fees are indicative and subject to change. Always confirm lender-specific terms before proceeding.

Choosing the right lender determines how much working capital you can get by pledging your property. When the LTV for loan against property aligns with your funding requirement, you avoid unnecessary financial strain

Higher loan eligibility helps you raise substantial funds without selling long-term assets or diluting ownership

Competitive interest rate structures reduce overall borrowing costs when paired with longer tenures

Flexible repayment schedules allow better alignment with business income cycles or long-term financial planning

Before committing, you should evaluate variables that influence both approval and sustainability of the loan against property.

Eligibility criteria differ across NBFCs and housing finance companies, especially for self-employed borrowers

Credit score quality directly impacts sanction terms, pricing comfort, and negotiation flexibility

Income stability assessment affects repayment tenure and the lender’s internal risk grading

A structured digital journey simplifies comparison and decision-making without repetitive paperwork. Bajaj Markets helps you evaluate multiple lenders through one guided flow.

Start with an online application by sharing property and income details accurately

Run a quick eligibility check to understand possible loan size and tenure options

Compare offers and proceed with documentation once terms align with your loan strategy

The LTV for loan against property should anchor your borrowing decision, not trail behind interest rates. When you align property value assessment, tenure comfort, and lender appetite, your loan strategy becomes predictable and resilient. Smart financial planning demands that you evaluate funding efficiency alongside repayment risk, ensuring the loan strengthens long-term stability rather than creating pressure.

The LTV ratio reflects the percentage of your property value that a lender sanctions as a loan amount, usually capped within regulatory limits.

A higher LTV improves liquidity and reduces the need for additional borrowing, making funding more efficient.

It enables larger funding against the same asset, supporting bigger financial goals without asset liquidation.

In some cases, lenders price higher LTV loans slightly higher due to increased risk exposure.

Most lenders extend financing up to 75–80% of the current market value of the property.

First-time borrowers may qualify, but credit strength and income stability remain decisive factors.

Higher assessed property value increases the absolute loan amount even when the percentage remains constant.

LTV revision post-sanction is rare and depends on reassessment of property value and borrower profile.

Higher leverage increases repayment pressure and reduces flexibility during income disruptions.

Compare tenure comfort, loan size limits, and fee structures alongside the indicative LTV range.

Yes, lenders usually apply lower LTV limits for commercial properties due to higher market volatility.

Most Viewed

Navigate the tax maze with ease! Uncover Income Tax 101, demystify jargon with Terms for Beginners, and choose between Old or New Regimes.

Unlock the world of credit! From picking the perfect card to savvy loan management, navigate wisely.

Money Management and Financial Planning covers personal finance basics, setting goals, budgeting...

Explore the investment cosmos! From beginner's guides to sharp-witted strategies, explore India's treasure trove of options.

Discover essential insights on various types of insurance in India.

Welcome to Tech in Finance, where we explore the exciting intersection of technology and finance...