Expense Tracking vs. Budgeting - Know The Difference

The rising popularity of cryptocurrency and the recent increase in responsible financial planning has attracted the interest of thousands, if not lakhs, of novices. However, if you’re new to personal finance management, then you need to quickly acquaint yourself with financial jargon. This will help you keep up with the market, financial practices, and any conversation surrounding finance.

You may have already come across terms like “Expense Tracking” or “Budgeting”. Unfortunately, one mistake beginners often make at the start of their personal finance journey is using these terms interchangeably.

So, before you begin to experiment with these terms, here’s everything you need to know about them.

Expense Tracking

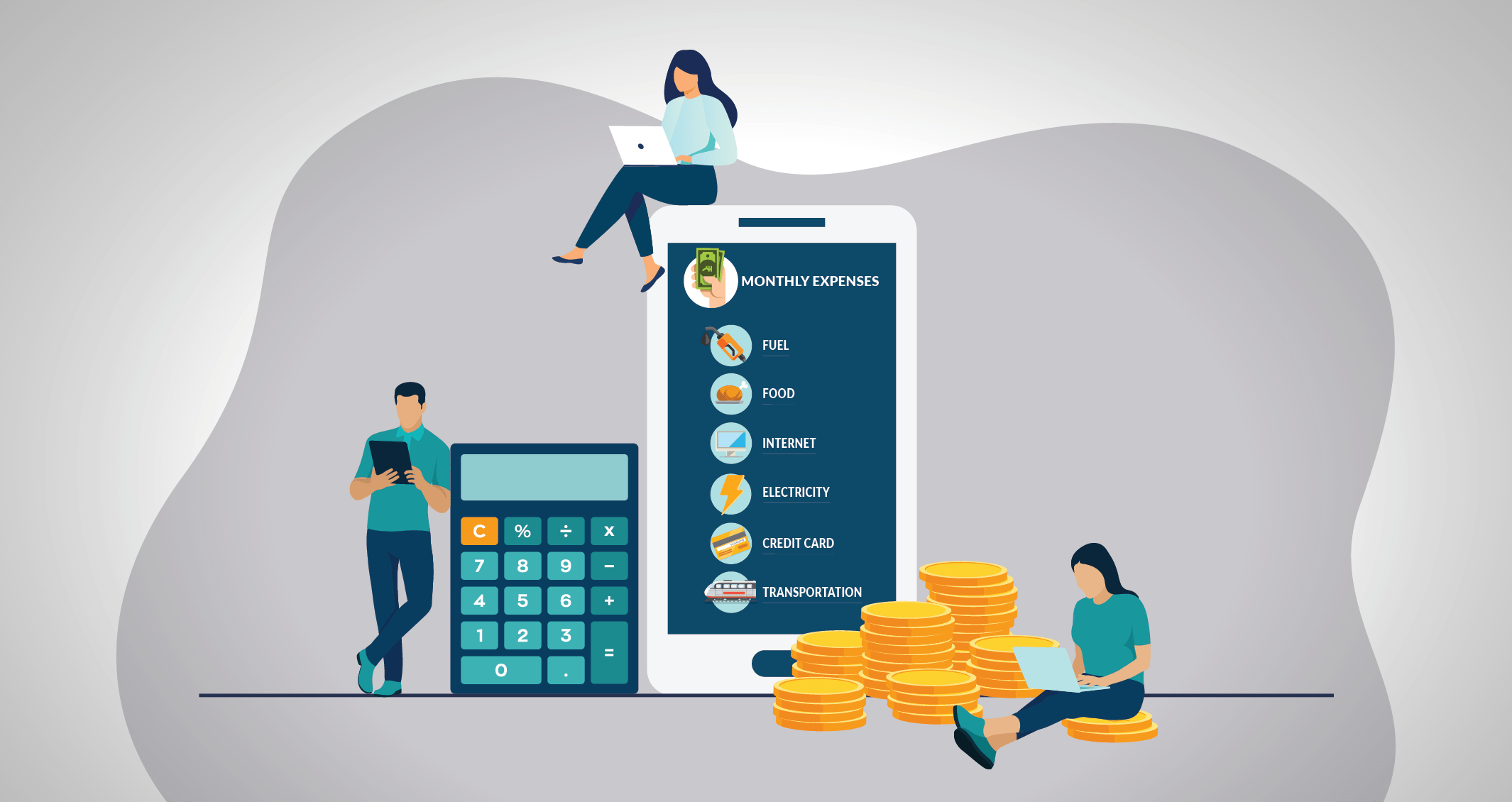

This is a crucial step to creating your budget, either for personal or business purposes. You can easily stay on top of your cash flow, and prepare for tax season by regularly recording all your expenses via receipts, invoices, etc. By monitoring all your outgoing expenses, you can create a budget that easily accommodates them.

Here are a few benefits of Expense Tracking:

- You develop a healthy habit of organizing your finances.

- Better grasp of areas with excess expenditure.

- It helps you track the progress of your personal finance goals.

- It motivates and encourages you by increasing your savings.

- You can avoid overspending and remain within the budget.

- Stops you from overindulging in impulsive purchases.

- Prevents you from adding anymore debt.

Additionally, by regularly tracking your expenses, you will be able to detect any unusual or fraudulent activity on your card/s.

Give expense tracking a try by using the following steps.

- Go through your account statements and list down your expenses.

- To gather an estimate, categorise them appropriately (e.g., groceries, subscriptions or fuel).

- Try to identity areas for improvement to reduce expenses.

Budgeting

Simply put, budgeting is the process of creating a plan to spend your money, after evaluating your income and expenses. By balancing the expenses with your income, you will be able to foresee areas for improvements and savings. In fact, the extra money you save can be put towards a steady investment plan to multiple your earnings.

Don’t miss out on these benefits of Budgeting.

- It helps you avoid the stress of going underbudget.

- You will be able to create an emergency fund (e.g., hospitalisation or loss of job).

- Enjoy financial freedom and independence.

- You can begin focusing on your own financial goals.

- Explore options of investment plans like Mutual Funds.

- Keeps track of all your income and expenses.

- You can control cash flow as you pay back debts.

Here’s another reason why budgeting is so important – Retirement fund! You will be able to successfully set aside a reasonable amount of money for when you reach retirement age. This in turn will help you focus on shifting budget to boost your savings.

Interested in creating your own budget? Follow these steps!

- Settle down and put together all your expenses, including recurring payments and debt repayment.

- List down all your sources of income.

- Subtract your expenses and income.

- If the remaining money is insufficient, evaluate your expenses and try to free up some extra cash.

What’s the consensus?

They aren’t the same! Expense tracking and budgeting serve different purposes, and so, you can’t use these terms interchangeably. Here’s the key difference between the two,

When you try to figure out where your money has been spent, this is called Expense Tracking. Whereas, Budgeting is when you try to create a plan for where money must be spent.

With this information in hand, you can avoid making novice mistakes while discussing financial topics. Just keep updating your repertoire of financial terms!

Blog Categories